Next stop 90%? Europe’s path to Net Zero in a Year of Elections

The European Commission’s level of climate ambition has ‘thrown down the gauntlet’ to politicians to show their colours on climate action during the European Parliament election campaigns in 2024. However, proprietary Penta data shows a significant drop in momentum regarding discussions around the EU Green Deal. Marie Donnelly, Senior Advisor, gives us her in-depth analysis.

Current opinion polls on the elections for the European Parliament (EP) in June 2024 point to a shift to the right with an increasingly vocal, real and/or opportunistic ‘greenlash’ to many policies aimed at meeting EU climate targets already legislated for under the Green Deal. Even further resistance is likely as a response to the Commission’s recommended climate target for 20401, and this was evidenced by a recent meeting of EU environment ministers, where just five of 27 Ministers openly endorsed the proposal.

It is clear that even a continuation of the current trajectory would be challenging in the face of political and popular reaction to existing measures, but as an interim milestone on the journey to a legally binding Net Zero in 2050, the European Commission has recommended a 90% reduction in the EU’s net greenhouse gas emissions by 2040 1 . The recommended target is a middle option and effectively means a continuation of the same pace of cuts as has been pledged for 2020-2030.

Public & Political Reaction

However, the EU is already struggling to meet the majority of its 2030 climate and energy targets and policy gaps abound post-2030. Over the coming months and maybe even years, Member States of the European Union will be called upon to agree (or not) on this level of ambition and the associated policies, legislation and financing support necessary to achieve the target.

Polls indicate that far-right parties will make substantial gains in the European Parliament elections in June 2024. This is likely to influence the EU’s policy stance on issues such as immigration, climate change and EU enlargement. In 2024 the political environment will be further influenced by a number of national elections , and current indications are that political fragmentation will be the outcome in many cases leading to an increasing share of coalitions or minority governments (perhaps the Netherlands, Portugal), some of which may need to rely on hard right or left parties (including Spain). This widening trend will most likely influence the positioning of the mainstream parties with visible attempts by them to ‘steal the clothes’ of both the far right and far left in election campaigns.

Greenlash takes hold

Popular resistance to climate measures, even those that are financially supported by Governments, have cooled many politicians’ climate ardour. In Germany, a public and political backlash to a contentious heating law (effectively a ban on all new domestic gas and oil boilers) led to a watered-down version being adopted and has weakened the ruling coalition.

Equally, farmers have been protesting across the EU, including in Belgium, France, Germany, Greece, Hungary, Italy, Latvia, Lithuania, the Netherlands, Poland, Spain and Romania. Whilst many of the farmers’ issues are directly related to climate action, some are not related at all, and several are based on policy measures that have not yet taken effect, such as the EU’s nature restoration law and a South American trade agreement. Nonetheless, farmer protests have already led to considerable softening of language on agriculture in the Commission’s 2040 Climate Target text.

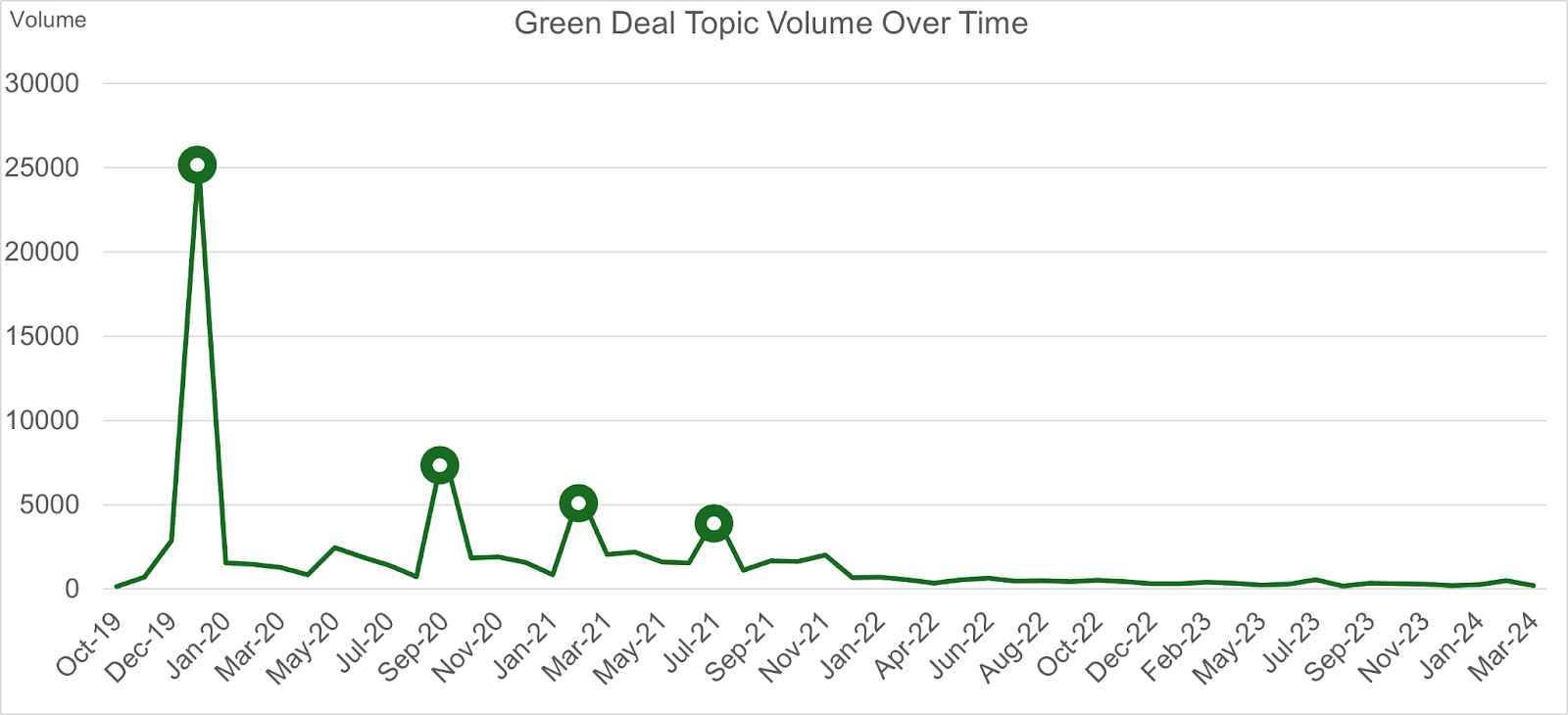

And as the EU gears up for the next European Parliament and Commission mandate, proprietary Penta data shows that momentum has left the European Green Deal in the public and political debate. At its grand unveiling in December 2019, the Green Deal captured the imagination of policymakers and the public alike, promising a greener, more sustainable future for Europe. However, what began as a wave of political enthusiasm, gradually ebbed over time, and was dealt a death knell with the beginning of war in Europe and rising inflation. As we approach the upcoming European Parliament elections in June in less than three months, there is little indication of renewed interest in the Green Deal, despite the finalisation of the EU’s landmark legislative initiative, the Fit for 55 Package.

Commission Ambition

Despite this disruptive political climate, in setting the direction to 2040, the Commission is sending the strongest policy signal and has started to set out a vision for a future Europe: confirming that fighting climate change would benefit citizens through improvements in air quality, ecosystems, enhanced health, and reduced healthcare costs whilst giving predictability for investments, and boosting the competitiveness of industries and economic resilience.

Implications of the 2040 target: Powering our way to 2040?

The Commission’s impact assessment shows how each economic sector would be called upon to play its part. Ambitious electrification is the foundation of the emission reduction / decarbonisation of the energy system by 2040. All zero and low carbon energy solutions (including renewables (especially solar and wind), nuclear, energy efficiency, storage, CCS, CCU, carbon removals, geothermal and hydro-energy, and all other current and future net-zero energy technologies) along with a further development of energy efficiency would be necessary to decarbonise the energy system by 2040. This would also require extensive roll out of smarter grids, system integration, demand flexibility and storage solutions. Energy system investment would need to more than double to €660 billion (equivalent to 3.2% of GDP) per annum on average.

Fossil-free future?

The corollary is that in 2040, the consumption of fossil fuels for energy would reduce by approximately 80% compared to 2021. This has significant implications for fossil fuel-dependent sectors, such as the oil and gas sectors, transport and energy intensive industries which would go through a fundamental transformation. It is expected that coal would be phased out, while oil in transport (road, maritime and aviation) would represent about 60% of the remaining energy uses of fossil fuels. The use of natural gas would be divided between industry, buildings, and the power system with fossil fuel combustion being coupled with carbon capture (utilisation) and storage. As a consequence, the gas market structure would change significantly, with an increasing role for low-carbon and renewable liquid fuels and gases, and gas infrastructure adapting to decentralized production. Repurposing the oil and gas network for e-fuels, advanced biofuels and renewable and low carbon hydrogen would need to be examined.

Bottling it up?

The target also requires a rapid deployment of zero and low carbon technologies by 2040, and concern has been expressed that this risks relying too much on technologies which are largely unproven, rather than prioritizing the cutting of fossil-fuel use. The assessment sets out a storage level of 280 million tonnes of industrial CO2 per annum by 2040 and a carveout to remove 75 million tonnes of CO2 from the atmosphere using engineering. To put this in perspective, the current total global capacity of carbon capture and storage (CCS) is around 40 million tonnes of CO2 with three-quarters being used for enhanced oil recovery (enhanced oil recovery (EoR)). Creating such levels at the EU level for carbon capture and removal technologies (e.g. BECCS, DACCS) which require significant future infrastructure development and investment, with uncertain social and ecological implications, could delay needed emission reductions and divert attention and resources.

A long road ahead

Projections on decarbonising transport vary greatly across transport modes. Estimated average annual investment needs in transport in 2031-2050 are estimated at about EUR 870 billion 2 . The acquisition of private cars represents the bulk of the investment needs in transport, accounting for around 60% of the total over the period although modal shift enables a decrease in the purchase of private cars. Reductions from road transport are expected to accelerate over time through the deployment of zero emission vehicles driven by the CO2 standards, and at least a quadrupling of the electrification of the sector over 2031-2040. The shares of battery electric and other zero-emission vehicles are projected to rise to over 60% for cars, over 40% for vans and close to 40% for heavy-duty vehicles by 2040. Beyond CO2 standards, carbon pricing and updated fuel policies would enable the decarbonisation of the stock of existing vehicles already on the roads that constitute the legacy fleet.

For the aviation and maritime sectors, the Commission would assess an extension of the carbon pricing in 2026. As part of this assessment, addressing barriers to the deployment of alternative low- and zero-emissions fuels (including e-fuels and advanced biofuels) in aviation and maritime and giving them priority access to these fuels over sectors that have access to other decarbonisation solutions such as direct electrification, is suggested to enable these sectors to contribute to the EU’s climate objectives and to the global climate agenda.

The elephant (or cow) in the room

Like all other sectors, agricultural activities play an important role in achieving the EU’s 2040 climate ambition although specific levels of emission reduction are not specified in the proposal. European farmers and foresters ensure the production of primary food and biobased materials, are at the core of the bioeconomy and the food system’s value chains and have a vital role in ensuring food security. As managers of the land, they are also essential to ensure ecosystem services such as biodiversity protection and restoration, carbon removals or adaptation to climate change.

A more generalised approach is taken in the Commission’s text, focussing instead on policies addressing the food sector in a holistic way rather than looking at the farming and fisheries sectors in isolation, because many decisions with a large mitigation potential are taken outside the farm gate: the chemical composition of fertilisers, the circular use of food waste (crop residues, manure, fisheries by-product), the reduction of food waste at the manufacture and retail stages, the choice of ingredients for manufactured food products, and consumers’ dietary choices. A whole-of-food-sector approach is therefore set out. Given that European agriculture is among the most efficient global producers of food in terms of greenhouse gas (GHG) emissions, there is a clear marker that the EU should also work to prevent unfair competition and to ensure a level playing field with non-EU producers, in particular through trade agreements.

All about the money, money, money

All routes to the 2040 target feature a shift in total costs from operational (linked to fossil fuel purchases) to capital costs. The macroeconomic analysis identifies overarching costs across all sectors and points out that investments of the order of EUR 470 billion of annual private funding would need to be mobilised. In this context, the 2040 target provides a guide to the financial sector and supervisory authorities when assessing the climate transition risks of investments, leading to favourable conditions when risks are minimised and adequate risk mitigation measures when they are not. Public support in the form of grants should only be strategically deployed to support early-stage low carbon projects such as renewable energy, in the industrial sector, and other projects, where projects lack commercial viability, private investment is still nascent and difficult to market investments.

It has become clear that as climate, economic and social challenges become more intertwined, they would need to be tackled as one to unlock the systemic change that would deliver progress in a just and resilient way. This includes investing in people through re-skilling and upskilling of the workforce, support for labour market transitions and targeted income support measures.

What’s next?

The next European Commission, to be appointed after the elections, would be tasked with proposing policy and legislation for this (or an alternative target) for member states and the European Parliament to debate in the years ahead.

As we stand on the brink of a pivotal moment in European politics, set to begin implementation of the Fit for 55 Package, the question is whether it’s next stop 90% on our journey to Net Zero.

1 The EU Climate Act requires the Commission to submit new post-2030 climate projections within six months of the global stocktake which was completed during December’s COP28 in Dubai, taking into account the advice from the European Scientific Advisory Board on Climate Change.

2 These figures represent the full acquisition cost of new vehicles, not only the incremental cost related to the decarbonisation of transport. In addition, it should be noted that investments in transport reflect here the expenditures on vehicles, rolling stock, aircraft and vessels plus recharging and refuelling infrastructure. They do not cover investments in infrastructure to support multimodal mobility and sustainable urban transport.